Social Security is commonly considered the “third rail” of American politics. As one of the most popular programs nationally, 87% of Americans indicate it as a priority regardless of the budget deficit.1 Maintaining Social Security is also a mainstay on the voting agenda of older Americans, who vote more often and thus have a greater effect on elections. Any mention of cutting or lowering Social Security benefits immediately receives backlash, as hard-working Americans do not want to be “cheated” out of the money they paid into social security throughout their lives. Given its popularity and effect on elections, politicians stay away from debates about reforming the current system. However, Social Security is facing a serious funding problem which needs to be addressed. According to the 2024 Annual Social Security and Medicare Trust Fund Report, the current tax level for funding Social Security is falling short of what the system needs to maintain current outputs, leading to the possibility of decreasing benefits and Social Security faltering over the next decade.2 In an attempt to alleviate the funding pressure and extend the life of Social Security, policymakers must jump on this political third rail and revise the current payment system if they want the current level of benefits to be around for future generations. Specifically, the federal government must raise or remove the cap on the payroll tax, which is the primary way Social Security is funded. The current tax is limited to the first $176,100 of earned wages, capping the amount of money that can feed into the system and disproportionately affecting lower wage earners.3 Although the cap increases slightly every year, adjusting to the average wage index, a raise or removal of the cap would provide more funding for Social Security benefits while also making the payroll tax proportional between low-wage and high-wage workers.4

The Current Social Security System, Its Shortfalls, and Its Importance

Social Security is an incredibly large program which is under significant stress and threat of decline. In fiscal year 2024 (when the tax was capped at $168,800), the federal government spent $1.5 trillion on Social Security for the elderly and people with disabilities, amounting to roughly 22% of the federal budget and making Social Security the single largest entity of federal spending.5 Retired workers and their dependents accounted for 78.5% of total paid Social Security benefits, paying out over 54.4 million people as of December 2024.6 To fund this massive program, roughly 184 million workers paid into the system, mainly through the payroll tax. Despite the pay going into Social Security, the funds supporting the program have consistently run a deficit – over the past three years, the assets that fund the retirement portion of Social Security have declined by approximately $170 billion in aggregate, depleting cash reserves.7 A May 2024 report from the Social Security Administration projects the primary fund for Social Security will deplete its reserves by 2035, and the fund specifically for retirement will run out by 2033. After depletion in 2035, funding from tax and interest sources would only be able to pay for 83% of Social Security costs.8 The funding problem is exacerbated as an aging population coupled with lower birthrates in the U.S. results in fewer young workers paying into Social Security for a growing number of elderly recipients.

Why the Government Must Act

It is important that the government responds to the financial problems Social Security faces and maintains its provision as Social Security provides a social safety net for individuals who fail to save for their own retirements. Although rational actors would typically save part of their wages for retirement without government intervention, this behavior is not observed historically or at the current time. Individual failures such as nearsighted savings behaviors, poor self-control, and lack of financial literacy and information lead people to poorly plan and save for their retirement. Nearsighted (defined by economists as myopic) savings behaviors occur when consumers think about short term desires and refuse to plan for the future. These individuals then choose to spend excessively in the present and forgo saving for tomorrow, leaving these individuals financially unprepared for retirement.9 Furthermore, many low-income households are forced to focus on day-to-day living and thus struggle to save for retirement.10 Poor self-control plays into this behavior as impulse spending in the present impedes future savings. Lack of financial literacy and information problems arise when individuals are unsure of how much to save for the future with one’s lifespan, future needs (especially medical needs for the elderly), and other factors being uncertain. The government stepping in to force savings through Social Security alleviates some of these economic failures of individual savings.11 According to a 2023 report, Social Security accounts for 50% of the income for 2/3 of retirees, while 1/3 of elderly households are almost entirely reliant on the program. In fact, without Social Security, 2/3 of the elderly would be considered in poverty.12 The safety net provided by Social Security protects these individuals who would otherwise be facing a financially uncertain retirement. Social Security is not a substitute for retirement savings, and the government could do a better job at encouraging individuals to save on their own. Additionally, one could argue a case for moral hazard in that Social Security itself incentivizes people to save less and that the government should take a hands-off approach on the issue of savings. Regardless, Social Security is already in place and has successfully protected some vulnerable populations, thus making it vital for the federal government to remedy its shortfalls in the interest of protecting these individuals.

The Payroll Tax and How Its Modification Can Help Social Security

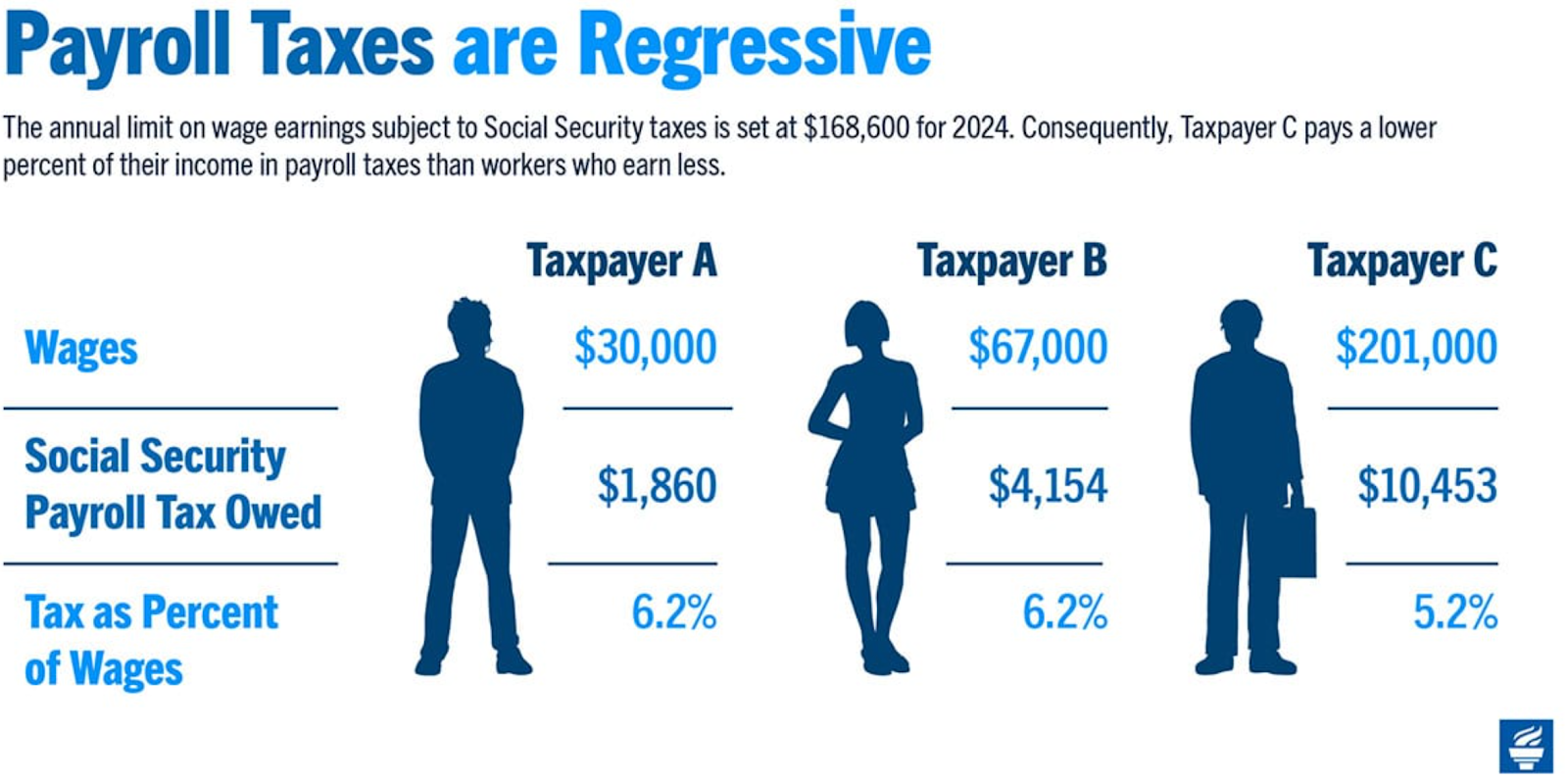

The primary funding for Social Security comes from a payroll tax through the Federal Insurance Contributions Act (FICA), which can be both progressive and regressive despite starting as a proportional tax. As part of FICA, employers and employees each pay a flat tax of 6.2% of the employee’s wage into Social Security funding, for a total of 12.4%.13 However, this tax structure does not apply to all of a person’s pay–a cap is applied which restrains the tax to the first $176,100 of wages (slightly adjusted each year), meaning someone making $176,100 a year pays the same payroll tax as someone making $1 million a year.14 By capping the taxable wage limit with a flat tax, the payroll tax shifts from being proportional to regressive, as high-wage earners above the cap pay proportionally less of their wages into Social Security than those earning below the cap (see Figure 1). Below the cap, the payroll tax is slightly progressive, as wages make up more of one’s income compared to other benefits as wages increase.15

Figure 1: The Regressive Nature of the Payroll Tax

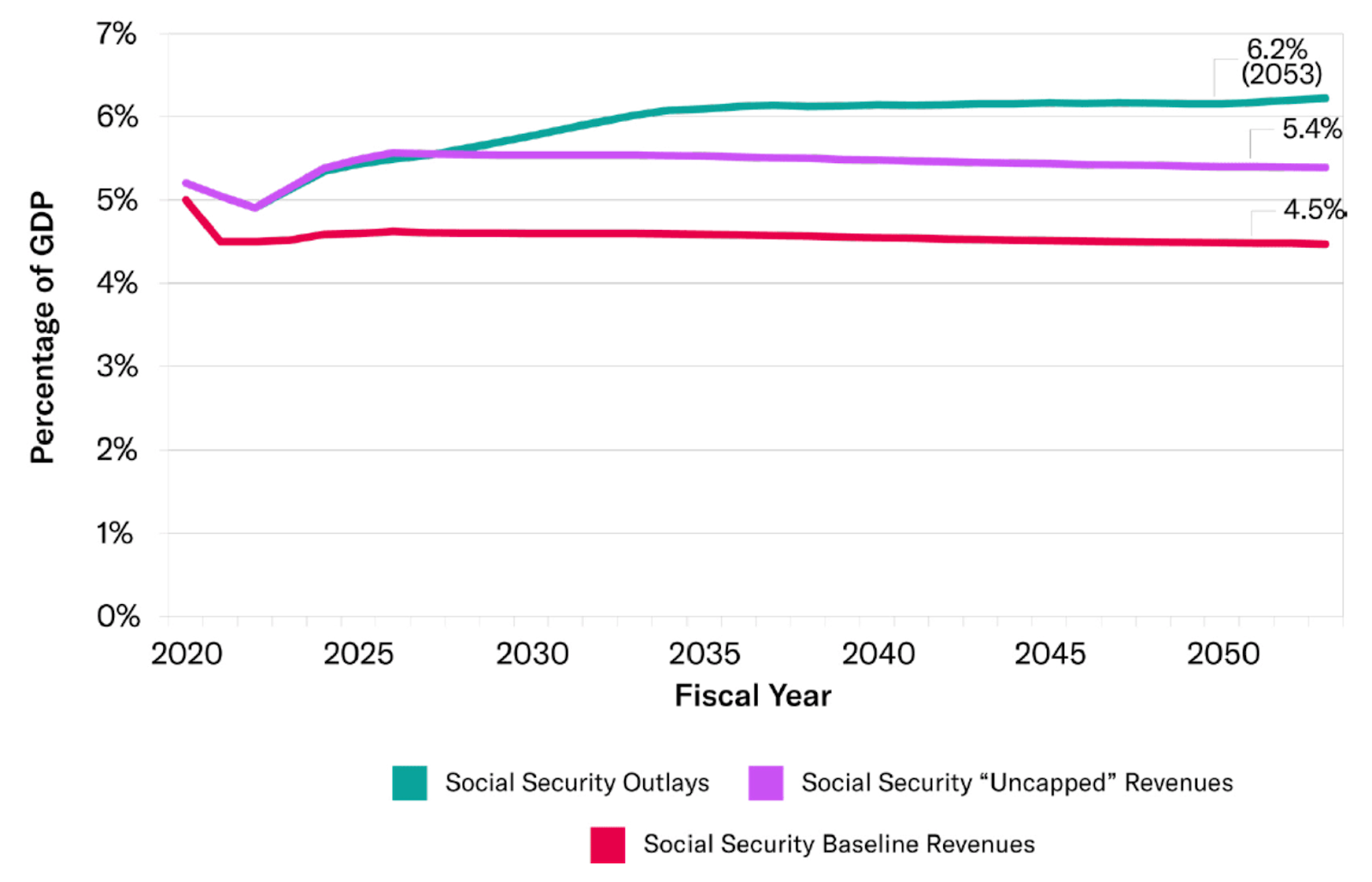

Modifying the payroll tax by either raising or fully removing the tax cap will expand the much-needed contributions to the Social Security fund and reduce the solvency issue. Since the 1980s, approximately 6% of workers consistently earn wages above the taxable maximum.16 In 2021, the top 5% of workers made up 29.9% of total wage earnings at an average of $322,349, more than 18 times the wages of the bottom 90%, and well above the payroll cap.17 Thus, with the current tax cap Social Security is losing out on a significant amount of potential revenue. Removing the cap would raise tax revenues from 4.5% to 5.4% of GDP, closing over half of the future gap of Social Security funding (See figure 2). Although not fully solving the financial gap, removing the cap would push back deficit spending to 2029 and reserve depletion from 2033 to 2055. If completely removing the cap may be too drastic a measure to undertake, even raising the cap would go a long way towards maintaining the future of Social Security.18

Figure 2: The effect of Uncapping the Payroll Tax

Tradeoffs and Economic Effects of Modifying the Payroll Tax Cap

As with any tax issue, modifying the payroll tax cap comes with tradeoffs and economic effects. First, the 6% of workers with wages above the current threshold would see a raise in taxes. The tax shift would lower these individuals’ take-home pay, changing their incentives and causing those affected by the tax to work less.. This shift away from work would lead to a decrease in supplied labor. However, since the tax increase would only affect 6% of workers, the overall effect on labor supply would be minimal, making this tradeoff less impactful. Furthermore, the decrease in take-home pay resulting from the tax would decrease current spending and overall economic output as workers adjust and lower their present spending habits. A cap raise also affects the employer’s behavior and tax incidence. As employers pay half of the payroll tax, removing the cap would also increase taxes on the employers of high-wage individuals. As a result, companies may pass some costs of the tax onto consumers. Raising the tax cap also affects the redistribution of Social Security funds. Part of the benefits structure of Social Security is that the more you pay into Social Security as a worker, the more you receive as a retiree. Therefore, raising the cap also raises the maximum amount of money Social Security can pay out. Thus, while raising the cap would provide more funding to Social Security, the increased payout of benefits would decrease the full effect of the extra funding.

The Future of Social Security

Clearly, Social Security is a vital part of the American social safety net that protects retirees and must be extended to provide for future generations. To do so, policymakers must stop fearing political backlash and take the important steps of reforming the current funding system. Raising or removing the payroll tax cap will not completely fix Social Security, but it is the first of many steps that can promote funding efforts and partially close the widening gap facing the program. Some in Congress are already starting to act on this idea: Senate Democrats led by Sen. Bernie Sanders (I-VT) have proposed the Social Security Expansion Act which, along with increasing benefits, would remove the tax cap on those making over $250,000. This “donut-hole” form of a cap raise would retain the existing payroll tax structure and then reintroduce taxes on wages for individuals earning more than $250,000.19 Proposed legislation like the Social Security Expansion Act are necessary considerations in order to remedy the funding structure before benefits are affected.

- Kenneally, Kelly, and Tyler Bond. “Americans’ Views of Social Security.” National Institute on Retirement Security, 22 July 2024, www.nirsonline.org/reports/socialsecurity2024/. ↩︎

- Social Security and Medicare Boards of Trustees. “A Summary of the 2024 Annual Reports.” Social Security Administration, 2024, www.ssa.gov/OACT/TRSUM/index.html. ↩︎

- Cardman, Michael. “2025 Wage Cap for Social Security Payroll Taxes Going up 4.4%.” Brightmine US, 23 Apr. 2025, www.brightmine.com/us/resources/talent-management/2025-wage-cap-for-social-security/. ↩︎

- “Contribution and Benefit Base.” Social Security Administration, www.ssa.gov/oact/cola/cbb.html. ↩︎

- “The Federal Budget in Fiscal Year 2024: An Infographic.” Congressional Budget Office, 20 Mar. 2025, www.cbo.gov/publication/61181. ↩︎

- “Social Security Fact Sheet.” Social Security Administration, www.ssa.gov/news/press/factsheets/basicfact-alt.pdf. Accessed 14 April 2025. ↩︎

- Williams, Sean. “Social Security Is Facing a $23 Trillion Funding Shortfall and Possible Benefit Cuts in 9 Years: Here’s How We Got Here.” The Motley Fool, The Motley Fool, 15 Dec. 2024, www.fool.com/retirement/2024/12/15/social-security-23-trillion-shortfall-benefit-cuts/. ↩︎

- Social Security and Medicare Boards of Trustees. “A Summary of the 2024 Annual Reports.” Social Security Administration, www.ssa.gov/oact/trsum/. Accessed 5 June 2025. ↩︎

- Kaplow, Louis. (2015). Government Policy and Labor Supply with Myopic or Targeted Savings Decisions. Tax Policy and the Economy 26(1), 159-193, https://www.journals.uchicago.edu/doi/full/10.1086/683367#_i1. ↩︎

- J.M. Jachimowicz, S. Chafik, S. Munrat, J.C. Prabhu, & E.U. Weber, Community trust reduces myopic decisions of low-income individuals, Proc. Natl. Acad. Sci. U.S.A. 114 (21) 5401-5406, https://doi.org/10.1073/pnas.1617395114 (2017). ↩︎

- Kaplow, Louis. Government Policy and Labor Supply with Myopic or Targeted Savings Decisions. ↩︎

- “Should We Eliminate the Social Security Tax Cap?” Peter G. Peterson Foundation, Peter G. Peterson Foundation, 13 Dec. 2023, www.pgpf.org/article/should-we-eliminate-the-social-security-tax-cap-here-are-the-pros-and-cons/. ↩︎

- “Topic No. 751” IRS ↩︎

- Ellison, Erin, and David Kindness. “What Is the FICA Tax? 2024 Tax Rates and Instructions.” OnPay, OnPay, Inc., 31 Oct. 2024, onpay.com/insights/what-are-fica-tax-rates. ↩︎

- “Are Federal Taxes Progressive?” Tax Policy Center, Urban Institute, Brookings Institution, and Individual authors, Jan. 2024, taxpolicycenter.org/briefing-book/are-federal-taxes-progressive. ↩︎

- “Population Profiles: Taxable Maximum Earners.” Social Security Administration, May 2024, www.ssa.gov/policy/docs/population-profiles/tax-max-earners.html. ↩︎

- Gould, Elise, and Jori Kandra. “Inequality in Annual Earnings Worsens in 2021.” Economic Policy Institute, Economic Policy Institute, 21 Dec. 2022, www.epi.org/publication/inequality-2021-ssa-data/. ↩︎

- Riedl, Brian. “Don’t Bust the Cap: Problems with Eliminating the Social Security Tax Cap.” Manhattan Institute, Manhattan Institute for Policy Research, Inc., 11 Apr. 2024, manhattan.institute/article/problems-with-eliminating-the-social-security-tax-cap. ↩︎

- “Lawmakers Announce Bill to Remove Social Security Tax Income Cap.” Taxnotes, 27 Feb. 2025, www.taxnotes.com/research/federal/legislative-documents/congressional-news-releases/lawmakers-announce-bill-remove-social-security-tax-income-cap/7rbl3. ↩︎